The story of Airbnb in Vancouver, WA is complex. By early 2024 the city capped short‐term rental (STR) permits at 870 units (1% of ~87,000 homes) (www.cityofvancouver.us). When the new rules took effect, about 425 existing STR hosts were identified and notified of the permit requirement (www.cityofvancouver.us). Third-party analytics confirm this modest scale: AirDNA estimated ~930 total STR listings in the area (all platforms) (www.airdna.co), while an Airbnb data aggregator counted roughly 499 active listings in late 2023 (www.airroi.com). In other words, even during Airbnb’s boom, STRs have been under 1% of Vancouver’s housing units. City officials note that although “STRs have risen over time,” Vancouver’s increase has been less dramatic than in bigger tourist centres (www.cityofvancouver.us).

Vancouver’s STR ordinance now tightens regulations. A one-time $250 permit (plus a business license) is required, and hosts must meet health/safety rules and notify neighbors. The code explicitly bans STR use in MFTE-subsidized housing (www.cityofvancouver.us). In effect, short-term rentals are only allowed in ordinary residences (owner- or tenant-occupied) meeting all building codes (www.cityofvancouver.us), and city data will be tracked quarterly. As of early 2026, the city hadn’t released updated permit counts beyond the initial figure, but watchers note only a few hundred owners signed up so far (well under the 870-unit cap).

Housing Inventory & Prices

Contrary to fears that Airbnbs would drain the housing supply, Vancouver’s market has actually loosened since the frenzy of 2020–21. In Clark County at large (which includes Vancouver), the number of homes for sale roughly doubled year-over-year by late 2025 (www.explorethecouve.com). Inventory sits at about 3.5–3.6 months of supply – roughly double the previous year’s level (www.explorethecouve.com). Houses now stay on market ~41 days on average (vs 26 days a year earlier) (www.explorethecouve.com). Sales volumes have barely budged (570 closed in Aug 2025 vs ~600 in Aug 2024 (www.explorethecouve.com)). In short, more supply has given buyers choice and slowed the once-frantic pace. Sellers are adjusting expectations (homes now close ~99% of list price, versus over 100% pre-pandemic (www.explorethecouve.com)).

All this suggests STRs are a relatively small factor in overall supply. Vancouver’s median home price is only modestly higher than a year ago – about $483K in Feb 2026, up just +0.7% YoY (www.redfin.com). That follows a ~flat market in 2025. By contrast, Downtown Vancouver (the historic core) saw median prices leap +24.7% over the same period – up to ~$503K (www.redfin.com). In far northwest Vancouver (near Salmon Creek), the trend was reversed: median price ~ $480K, down 8.1% YoY (www.redfin.com). These neighborhood snapshots show wide variation (and no obvious single cause).

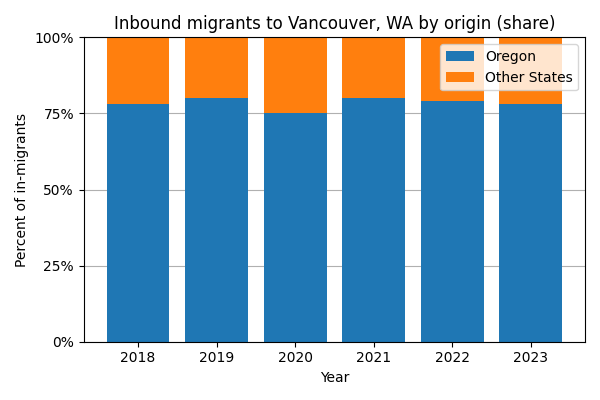

One take: Airbnb demand appears strongest in central, tourism-oriented areas, which also had tight supply, so prices spiked there. In outlying “starter-home” suburbs, prices cooled as inventory grew. Strikingly, a typical Vancouver Airbnb host earns only modest rental income: about $26,200 per year (www.airroi.com) (median gross revenue per listing), with average occupancy ~51% (www.airroi.com). That’s far below full-time lodging; it points to many hosts renting spare rooms or occasional use rather than running a full hotel. From the demand side, most new residents are still commuters and transplants: mobility data show roughly 75–80% of Vancouver’s inbound movers come from Oregon, a stable pattern each year (advanresearch.com) (chart below).

Who Gets Zoning and Who Doesn’t

Vancouver’s rules create clear imbalances in where STRs can appear. With the MFTE ban (www.cityofvancouver.us), none of the city’s new affordable apartments can be used as Airbnbs. In practice that means high-rise urban projects and subsidized housing stay reserved for year-round residents. STRs instead concentrate in ordinary homes and small multifamily buildings citywide. Because all STRs must be in legally established dwellings (no detached cabins or RVs), the densest STR clusters are likely in residential neighborhoods near downtown or parks. Exact location data for Vancouver STRs aren’t public yet, but similar cities show heavy clustering around downtown cores.

Anecdotally, owners in older neighborhoods (west Hough, downtown, Lake Shore) actively listed on platforms, whereas newer subdivisions are mostly stable family homes. This zoning gap has stirred debate: year-round families vs short-term hosts. Some argue that every STR unit is “one less house” for a local family. But the data suggest scale matters: with only a few hundred STR units, the overall effect on housing stock is fairly small. Indeed, Vancouver’s recent housing policy reflects this balance — the city passed an Affordable Housing Levy in 2023 (Prop 3) to fund 2,400 new affordable units (www.cityofvancouver.us), recognizing broader needs. Meanwhile, even as Airbnb activity grew locally, long-term rental rates and vacancy have not plunged, and survey data (Census/ACS) show Vancouver’s renter vs owner mobility statistics are broadly stable.

Insight – Year-Round vs Starter Homes: Vancouver’s STR debate often pits built-out owner neighborhoods against new first-time-buyer areas. Consider how prices moved: in downtown (mostly established neighborhoods) prices jumped ~25% (www.redfin.com), whereas in a growing starter-home suburb (Salmon Creek) they fell ~8% (www.redfin.com). One interpretation is that influx of tourists and part-time visitors bid up prices in amenity-rich zones, while outer “starter” markets had more supply and cooled off. From a community view, defenders of year-round housing point out that each STR license grants above-market returns (average host ~$26K/year (www.airroi.com)) that encourage investment over occupancy. Proponents of “starter home” housing note that protecting programs like MFTE (www.cityofvancouver.us) and building more affordable units can mitigate any displacement. In short, STRs may boost some owners’ income, but so far they remain a niche in Vancouver, unlike crises seen in bigger tourist cities.

What’s Next – Policy and Politics

Vancouver’s response has been cautious. The 24-month STR pilot launched in 2024 is still underway, and officials are watching how permits fill up to the 870-unit cap (www.cityofvancouver.us). If permits are not exhausted, the city may leave them unused, limiting STR growth. Meanwhile, modest platform growth (+3% new listings last year (www.airdna.co)) and occupancy ~51% (www.airroi.com) suggest no explosion of vacation rentals. Any local impact on hotel or motel tax revenues will be minor; Vancouver’s lodging tax committee continues funding tours and events, often citing state revenues laws (www.cityofvancouver.us).

On the political front, voters have already signaled housing concerns. In 2023 they approved a major affordable-housing levy (www.cityofvancouver.us). The STR issue itself sparked extensive public input in 2022–23 (the city heard from 57 people in one evening on an unrelated streets initiative (www.cityofvancouver.us), showing build-up interest in local land-use issues). With city council elections coming in late 2025, housing questions – from density to rentals – are sure to be on the table. For now, the verdict is that Airbnb’s footprint in Vancouver remains modest: clearly neither trivial nor overwhelming. Planners will continue to weigh any so-what: balancing owners’ extra income against the goal of keeping homes for year-round residents. The data so far suggest Vancouver has largely succeeded in keeping that balance within reasonable bounds.

Sources & Metadata: Vancouver city policy releases and code (City of Vancouver, 2023–24) (www.cityofvancouver.us) (www.cityofvancouver.us) (www.cityofvancouver.us); Airbnb/STR analytics (AirDNA/STRProfitMap/AirROI, 2024–25) (www.airdna.co) (www.airroi.com); housing market data (Redfin, Feb 2026) (www.redfin.com) (www.redfin.com) (www.redfin.com); Clark County market report (Sep 2025) (www.explorethecouve.com) (www.explorethecouve.com); migration and survey info (Advan 2018–23; ACS not shown) (advanresearch.com); Vancouver affordable-housing levy (Prop 3, Feb 2023) (www.cityofvancouver.us).

About the Author

The Holloway Team is comprised of seasoned professionals dedicated to delivering unparalleled real estate experiences. Lauren, a top-producing agent at Compass, brings a wealth of expertise to ensure a smooth and stress-free experience, making your journey as effortless as possible. Henry, as our Data Analytics expert, provides actionable insights to drive informed decision-making in the real estate team. As a team we stand out as the preferred choice for clients seeking a seamless real estate experience in Southwest Washington.